Blockchain Implementation: Market Stats

Satoshi Nakamoto developed blockchain technology to support the exchange of digital currencies. But the tech-savvy world quickly saw that blockchain implementation could be applied to develop corporate apps. In 2018, the global blockchain market was estimated to be worth 1.57 billion dollars. By 2027, that figure is expected to have increased more than one hundred-fold to 163 billion dollars.

The use of blockchain technology has the potential to improve daily transactions’ efficiency, trust, and transparency. As a result, business executives are already organizing crucial projects for their companies. Blockchain technology is developing quickly across industries and is now incorporated into the company’s transformation process.

Therefore, this blog will discuss how businesses can implement blockchain in their enterprise apps. Moreover, we will also talk about a few examples of how some successful companies are also using a similar module.

Things Businesses Must Consider

Integration of blockchain technology is complex. While going through this process, businesses should keep a few things in mind.

1. Refuse To Give In To Setbacks

The blockchain implementation protocols will only ever work to their full potential right away in any way. Please make a copy of all the errors and problems, then attempt to correct them.

There are various ways to do this, but businesses should keep the blockchain as straightforward as possible. Remember that your best friends are trial and error. Make sure businesses perform enough trials and view each as a critical step along the learning curve.

2. The Implementation Must Be Successful

A business must thoroughly and properly test its system to ensure it functions as intended. It is imperative to conduct testing initially in a controlled environment. The real-world testing then starts. Businesses might discover a few unusual factors they had not thought of before. Any such element could impact the outcomes of their blockchain deployment.

3. Make The Future Idea

Preparing for the next step would be best as soon as businesses develop a functioning blockchain implementation protocol. Examine a few areas that want improvement. For future growth requirements, businesses can also keep an eye on the scalability of the blockchain. It is essential to prevent the stagnation of technology. A never-ending pursuit of excellence through incremental improvements.

Case Studies: Businesses With Successful Blockchain Implementation

Two blockchain case studies are presented in this article. Business Executives may learn how to integrate blockchain into the company by using real-world examples.

1. Nestle

Blockchain verifies the quality of baby products.

Business Provocation: In 2008, melamine poisoning from powdered milk products harmed 300,000 neonates. Chinese parents’ faith in newborn nutrition items was shaken. Nestle was looking for ways to persuade Chinese parents of the superiority of its infant feeding product, NAN A2, to enter the market successfully.

Action: To develop a public blockchain platform that works with a mobile app, nestle collaborated with a Chinese technology company. As a result, parents can use their phones to confirm the following features of the NAN A2:

- Constituent: Place of purchasing the ingredients

- Production origin

- Packaging information, including pictures

Outcome: As a result, Nestle owned the most significant market share in China’s infant nutrition market thanks to the transparency offered by blockchain. Nestle knows very well how to implement blockchain in business.

2. Etherisc

Instant claim processing is ensured via blockchain.

Business Test: Etherisc is a startup in the insurance industry. Etherisc was seeking ways to expedite the claims processing. The traditional claims processing process often takes weeks to resolve a claim, albeit the length of time depends on the insurance carrier and the type of claim. According to EY, almost 90% of insureds base their insurance selection on the caliber and efficiency of the claims handling procedure.

Action: Automate the handling of claims. Etherisc uses blockchain technology to enable smart contracts, which enforce agreements when predetermined criteria are satisfied.

Outcome: Shortens the time needed to settle claims. Automatically examines potential fraud utilizing information from outside sources.

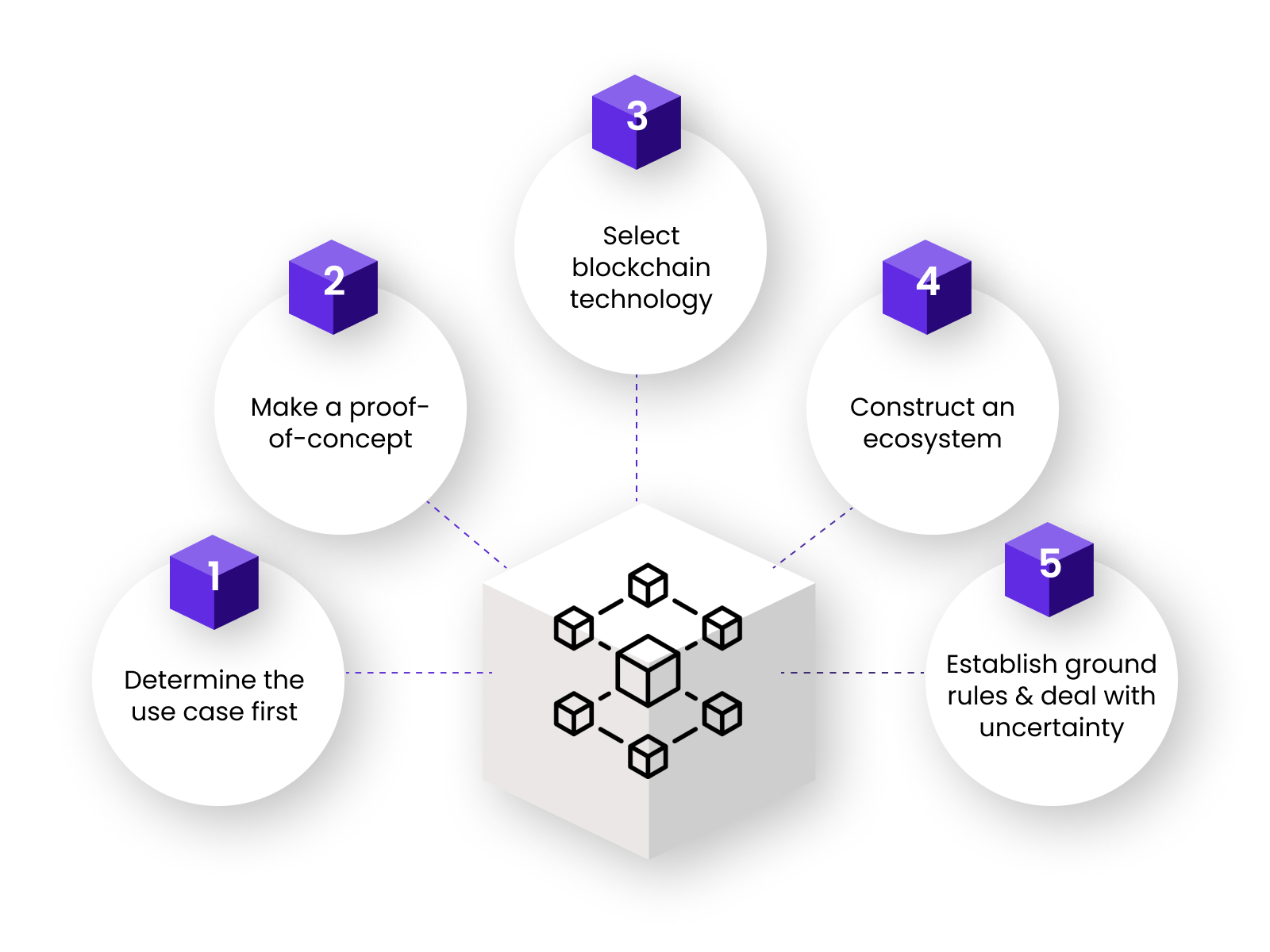

5 Steps For Successful Blockchain Implementation

Blockchain Implementation Step 1: Determine The Use Case First

Identifying, outlining, and organizing your needs comes first. Determine whether applying blockchain technologies will assist in the resolution of the specific issues businesses wish to solve. It is advised to begin with a pilot project, evaluate the outcomes, and then put them into practice on a bigger scale.

Blockchain Implementation Step 2: Make A Proof-of-Concept

Having defined the use case, producing a reliable Proof of Concept (POC) is essential. PoC is nothing more than a tactical technique to assess whether blockchain would be practical for the company. Businesses can develop their Proof of Concept by following the evaluation and planning phases.

Blockchain Implementation Step 3: Select Blockchain Technology

Consider choosing blockchain technology implementation based on the technical staff organization and open-source station. The platform should accommodate the budget. However, moving from a fruitful proof of concept to a comprehensive blockchain implementation is difficult for governments and businesses.

Blockchain Implementation Step 4: Build An Ecosystem

When stakeholders participate, blockchain technology performs at its best. However, an organization’s community is required to build a new industry ecosystem. It can strengthen norms and laws by comprehending the possibilities of technology.

Blockchain Implementation Step 5: Establish Ground Rules & Deal With Uncertainty

Using blockchain to implement the new ecosystem should solve the organization’s problem. Moreover, businesses must address issues like cybersecurity, compliance, and privacy.

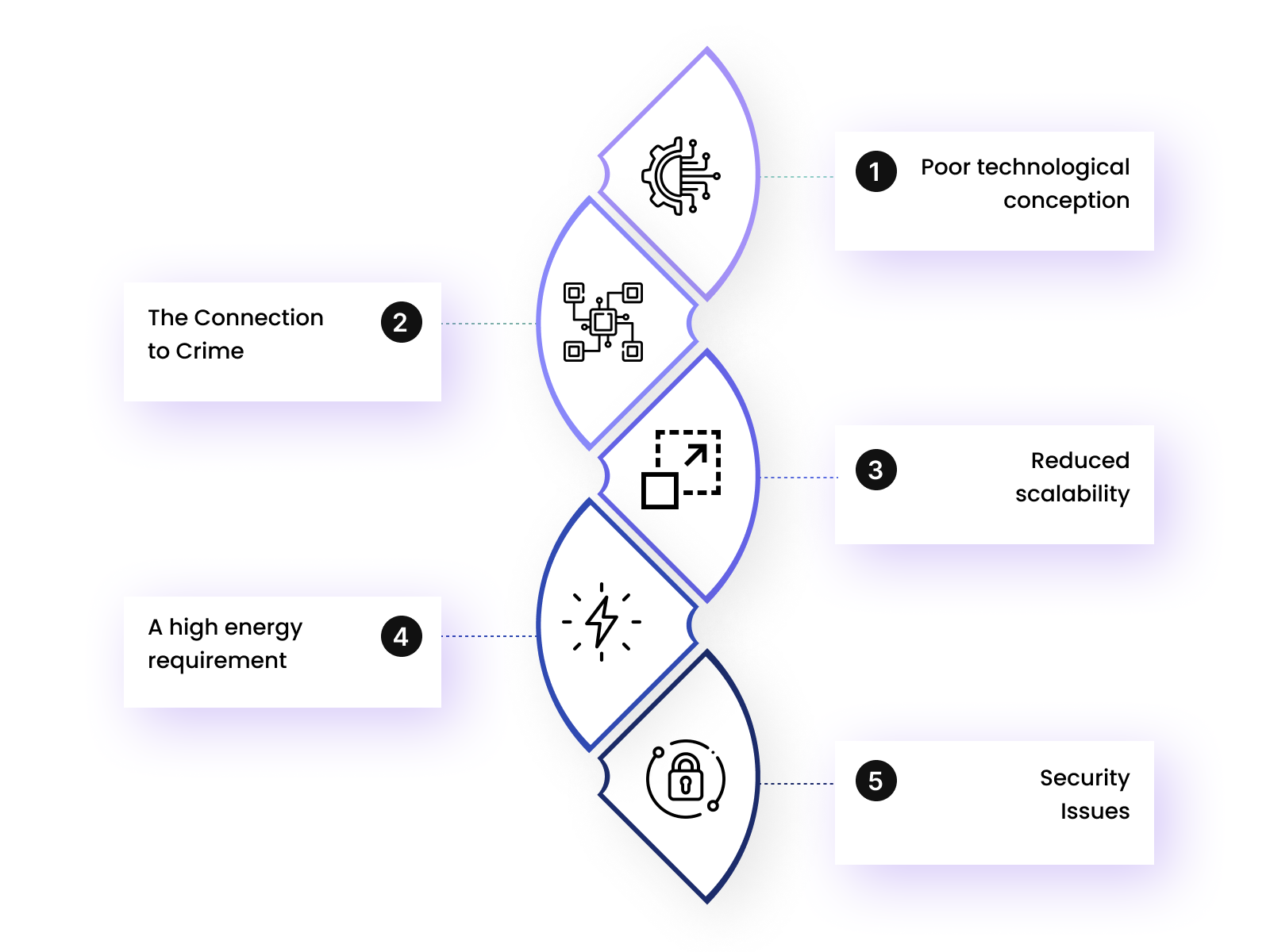

Possible Challenges: Businesses Face

1. Poor Technological Conception

One of the main difficulties in deploying blockchain is this. Despite its many benefits, blockchain technology still has a lot of technological shortcomings. Additionally, one of the essential aspects of this is a bug or loophole in the program.

2. The Connection To Crime

Academics and criminals were drawn to blockchain implementation adoption because of its anonymous nature. Why? Since the network is decentralized, nobody can determine the genuine identity. Due to this, bitcoin is the main currency used on the dark web and in illicit markets.

3. Reduced Scalability

Scalability is another issue with blockchain implementation. In practice, a tiny percentage of users can successfully use blockchains. But what will happen if there is a mass integration? Ethereum and Bitcoin have the most network users and struggle to manage the load.

4. A High Energy Requirement

Another issue with blockchain deployment is energy usage. As with Bitcoin, most blockchain technologies feature Proof of Work as their consensus mechanism. Businesses need to use their computer to solve challenging mathematics problems while mining. As a result, once they start mining, the PC will require more electricity.

5. Security Issues

Another critical issue, in this case, is Security. Robust Security is the main feature of blockchain application development. However, like every other technology, blockchain has a few security flaws.

One of the network’s security holes is the 51% attack on it. In this attack, hackers can seize control of the network and use it to their advantage. Consequently, they have the power to modify transactions and prevent others from forming blocks.

Markovate’s Expertise In Blockchain

Markovate develops enterprise blockchain solutions and controls smart contracts and cryptocurrency wallets using blockchain implementation. It offers end-to-end blockchain development services to produce safe, scalable, and interoperable dApps.

It also integrates immutability, decentralization, and transparency into blockchain services.

Blockchain Implementation: FAQs

1. Is blockchain easy to implement?

Implementing a straightforward blockchain solution like a Bitcoin token system is relatively easy. Implementing a more complicated system, such as one that automates supply chains utilizing blockchain technology and smart contracts, is more complex.

2. How much does it cost to build a blockchain?

Developers can create Blockchain apps on a variety of blockchain networks. However, on these networks, the costs for developing dApps range widely. Developers spent approximately $6,000 to $400,000 developing applications on Hyperledger Fabric, Ethereum, EOS, and Ripple blockchains.

3. What apps use blockchain?

Blockchain applications go well beyond cryptocurrencies like bitcoin. For instance, several applications use blockchain, including Chainyard, Voatz, Burst IQ, TraceDonate, and KYC-Chain.

Further read about the top Blockchain development companies!